It is a common story: a family member wants to help a young entrepreneur get their business off the ground by financing a major purchase—like a van or specialized equipment. However, as one recent case illustrates, good intentions without proper tax planning can lead to a complete loss of tax relief.

The Scenario

A father wanted to support his 20-year-old daughter’s new landscaping business. She needed a reliable van, but as a new business owner, she couldn’t secure a competitive loan.

The father stepped in, took out a personal loan, and purchased the van in his own name. The daughter used the van 100% for her business and agreed to reimburse her father monthly to cover his loan repayments. On the surface, it’s a perfect family arrangement. In reality, it created a “tax vacuum.”

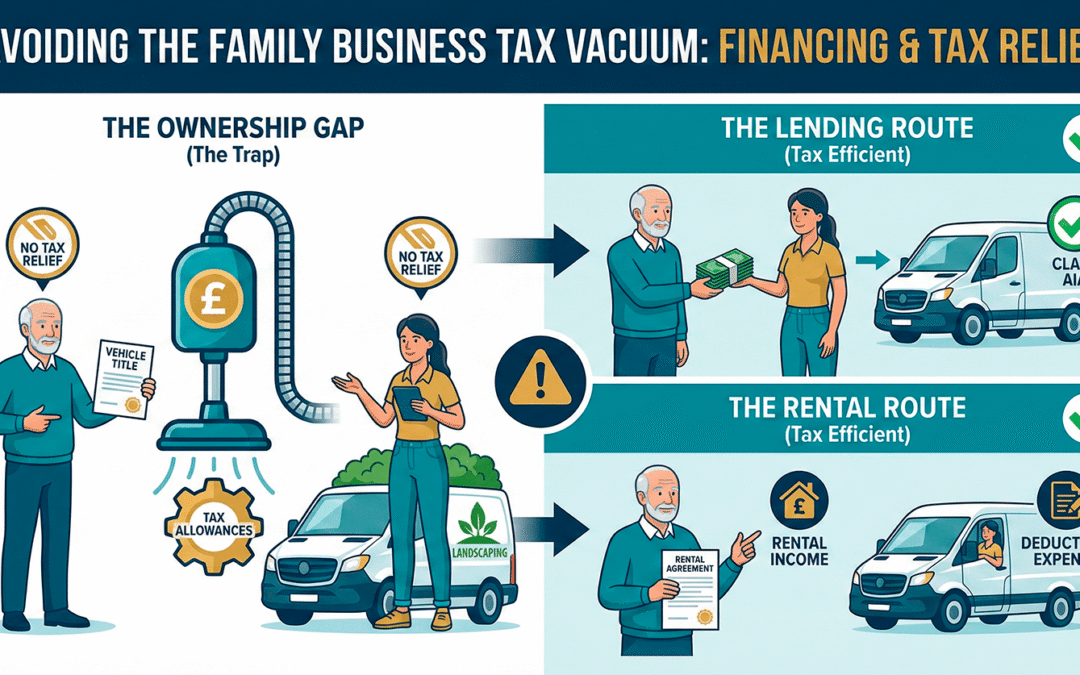

The Problem: The Ownership Gap

To claim Capital Allowances (CAs)—the tax deduction that allows a business to write off the cost of equipment—the claimant must generally meet two conditions:

- They must own the asset.

- They must use the asset in their trade.

In this case:

- The father owns the van but has no business, so he cannot claim.

- The daughter uses the van for business but does not own it, so she cannot claim.

The “Contribution” Trap

Tax rules do sometimes allow a person to claim relief if they “contribute” to the cost of someone else’s equipment. However, for family businesses, there is a major catch. Relief is blocked if:

- The original purchaser (the father) wouldn’t have been entitled to claim anyway.

- The two parties are “connected” (e.g., parents and children).

Because they are family, the daughter cannot claim relief on the monthly reimbursements she makes to her father. The result? A £30,000 van is used for business, but £0 of tax relief is claimed.

How to Avoid the Trap

If you are looking to help a family member finance business equipment, there are two main ways to ensure tax efficiency:

- The “Lending” Route: Instead of buying the van yourself, lend the cash to the business owner. They use the cash to buy the van in their own name. They now own the asset, use it in their trade, and can claim the Annual Investment Allowance (AIA) to write off the full cost immediately.

- The “Rental” Route: If you have already bought the asset, draw up a formal commercial rental agreement. The “reimbursement” then becomes a tax-deductible rental expense for the business (though the parent would then need to declare this as rental income).

The Lesson

Before signing for a loan or purchasing an asset for a family business, always ask: “Who will own this for tax purposes?” A quick conversation with your tax advisor beforehand can prevent a very expensive mistake.

Disclaimer

This article is for illustrative purposes and provides general information only. It does not constitute professional tax or legal advice. Capital allowance rules are complex and depend on the specific legal structure of the parties involved. Please consult with a qualified professional before entering into any financing or purchase arrangements.